Today we’re going to look into Index Funds vs ETFs vs Mutual Funds, the similarities and differences between them, pros and cons of using each of these funds and what you actually need to know about them. If you are confused at all about these different investment types and are trying to figure out which one might be the best for you, be sure to read right to the end, as this post will be really helpful for you and is full of important details.

It’s actually really common for investors to get mixed up between Index Funds vs ETFs vs Mutual Funds, and even though they are all types of investment funds they’re actually very different to each other. So when I hear people use Index Funds and ETFs interchangeably it really makes me cringe a bit, Index Funds are not the same as ETFs please don’t make this mistake. And it’s going to be important you guys pick the right one for yourself from the start, as it can be costly and annoying to change later on, which is actually what happened to me. I want to save you this trouble!

Now with that out of the way let’s get right into the nitty gritty. So to start with there’s a lot of similarities and benefits that are common between Mutual Funds, ETFs and Index Funds, which I’ll outline before deep diving into each fund type.

Common Benefits of Index Funds, ETFs and Mutual Funds

All of these funds offer two major benefits: the first is convenience. By investing in a Mutual Fund, Index Fund or ETF you get to own a bunch of different companies all in one easy package. One of these funds could have thousands of different individual stocks in it but you only have to make one purchase to own a portion of all of them. In a world without funds, if you wanted to have say a thousand different stocks in your portfolio you’d have to make 1000 separate purchases. If you’re paying $10 per trade that would cost you $10,000 alone just buying the companies, it would also take you a lot of time! However depending on the fund you chose you would either pay nothing to enter the fund or just pay a one-time fee. This is way simpler than trying to self-manage a portfolio of thousands of different companies, constantly trying to re-balance weightings every day.

Through owning a lot of different stocks this gives you the other major benefit of these investment funds, that is diversification. Like even if you have 10 individual stocks in your stock portfolio if one of those goes down and fails you can end up losing a lot of money. On the other hand if you go and buy the entire S&P 500 index fund, then you have 500 different stocks and different companies that contribute to your overall return. So even if one of those fails it doesn’t really matter because you have 499 others to boost you up.

This means that having a few individual companies go up or down in the markets in the short term won’t really affect your overall return because you’re betting long term that the market will rise overall as a whole. Also doing this as an investor will give you a lot more market stability because let’s be real most people can’t handle the market volatility and as soon as they see it go down they panic and they freak out and they sell it and then they see it going back up and they buy back in because it’s going back up now. Then they have literally done the worst thing in investing, which is to buy high and sell low. That’s why investing in Index Funds, ETFs and Mutual Funds solves most of those issues.

Mutual Funds

So I’ll start with mutual funds which were the original investment fund out of these 3 types and have been around the longest. A mutual fund is a type of investment product where the funds of many investors are pooled into an investment product. The fund then focuses on the use of those assets on investing in a group of assets to reach the fund’s investment goals. Now it’s important to note here, by pure definition a mutual fund can actually be either an actively managed fund or a passive index fund, but industry-wide it’s widely assumed when someone is referring to a mutual fund these days, they are talking about an actively managed fund and for simplicity’s sake I will be using the same assumption when talking about mutual funds now.

The simplest way to think about mutual funds is, imagine you have this super smart friend who is great at picking stocks and you see they are making lots of money all the time. Then you think to yourself, wow I wish I could just give my money to my friend so he can invest for me as well. Now imagine your friend isn’t the nicest friend and then tells you he is going to charge you a fee for his services, and then he also tells you that this fee will need to be paid regardless of whether he actually makes you any money or not (and he isn’t going to guarantee to make you money). Then imagine your friend is actually not nice at all and tells you that if he does actually perform really well and gets you a good return, well then he will charge you an additional “performance fee”! Well if you’ve got that pictured in your head, that’s pretty much what a mutual fund is.

Active-management

Mutual funds are typically “actively managed” which means that they have a person, usually a fund manager, who will be actively trading the portfolio of investor funds to achieve the investment goal of the fund. The investment goal is usually to achieve a return that is greater than the overall market, but that’s just it, it is a goal and it rarely actually happens.

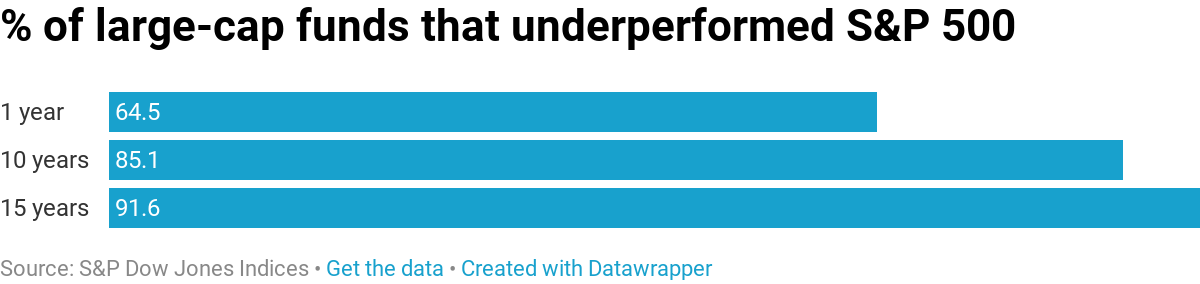

In a report released by S&P in 2019 on how actively managed funds performed against their benchmarks. It showed that active managers continue to show dismal performance against the overall market. For the ninth consecutive year, the majority (64.49 percent) of large-cap mutual funds lagged the S&P 500. And that’s just over a 1 year period, when looking at the data over longer periods this gets really dismal. Over a 15 year period less than 9% of active mutual funds were able to outperform the S&P 500.

However there is still a non-zero chance you are able to find a mutual fund that is able to beat the market however in return for managing your money actively managed mutual funds charge an annual fee of typically 1-2% of your account balance every year. So at 2% if you invested $10,000 in a mutual fund, $200 of that goes straight into the fund managers pocket. Even if the manager makes poor investment decisions and your account balance actually goes down next year, you still get charged 2%. You could literally end up with less money than you started with But the fund manager would still get paid millions of dollars for their services. Over the years fees will reduce your nest egg by hundreds of thousands of dollars. So the vast majority of mutual funds are probably not worth the higher fees.

Mutual Fund Liquidity

The final point I want to make about mutual funds is how you actually invest in them. These aren’t like shares which are traded on the stock market, they will normally have a website setup where you can create an account and then transfer cash directly into the investment fund. This is usually a bit more clunkier than buying and selling through a stock exchange so your money is going to be a little less liquid when using a mutual fund and is something to note if you want fast access to cash. They will also usually have a minimum balance requirement in order to open an account which makes it harder to get started which is something to consider when evaluating Index Funds vs ETFs vs Mutual Funds.

Index Funds

Moving on to Index Funds which are actually a type of Mutual Fund that were born out of the desire for low fee passive index tracking funds, and this created the Index Fund. Like the name suggests, Index Funds are always passively tracking an index. If you don’t know what an index is: it’s a method to track the performance of some group of assets in a standardized way. Indexes typically measure the performance of a basket of securities intended to replicate a certain area of the market. These may be broad-based to capture the entire market such as the Standard & Poor’s 500 (S&P 500) or Dow Jones Industrial Average (DJIA), or more specialized such as indexes that track a particular industry or segment. Indexes are also created to measure other financial or economic data such as interest rates, inflation, or manufacturing output.

Tracking Error

So Index Funds are similar in a lot of ways to Mutual Funds except that the fees will be much lower because there isn’t a fund manager actively trading the fund. As a consequence the performance of the Index Fund will closely mirror the index it is tracking and you won’t get any potential out performance of the index. A unique component of index funds because they are tracking an index, is a thing called “tracking error” and this is basically the Index return – index fund return = tracking error.

The management fee you are paying when you choose to use an Index Fund is essentially paying them to make sure that they track this index as close as possible and that’s pretty much it. Therefore if an index fund is good at tracking an index then this tracking error should be equal to their management fee, if it’s a lot larger than their management fee then you should probably consider it’s a good Index Fund to be using as they aren’t doing what you are paying them to do.

Low-fees

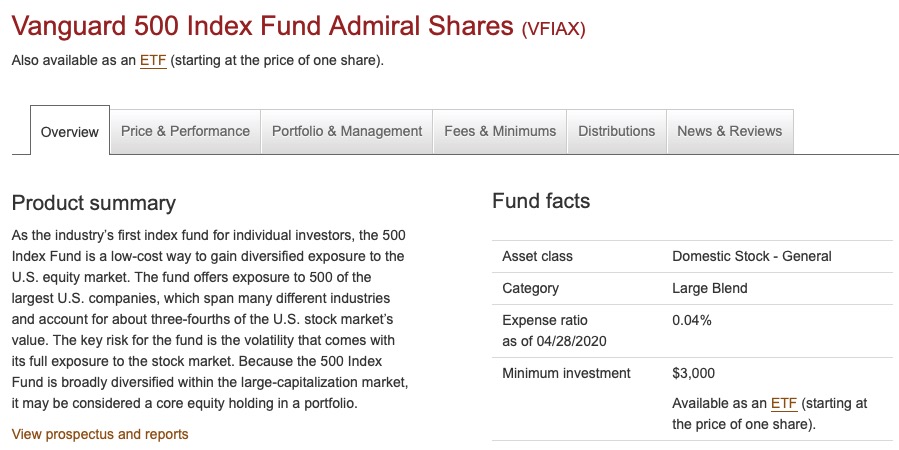

With Index Funds because there is no team of stock pickers or a highly paid Wall Street expert that’s choosing which stocks to include in the fund the fees are much lower than with an active Mutual Fund. For example one of the most popular Index Funds in the world and actually the first ever index fund for individual investors, Vanguard’s 500 Index Fund in the US has a management fee of only 0.04% p.a, which is incredibly low when compared to active funds which are usually above 1%, over 25x higher!

Passive Index funds really are great for most individuals, as most investors out there will make more money investing in an index than they would investing in individual stocks on their own. Several studies have shown that over 90% of portfolio managers could not outperform the market index over a 15 year period. And keep in mind that these are people who are the brightest in their field who have gone to Ivy League schools with a really deep understanding of economics and finance who do this full-time daily and not even they can outperform just the market index.

And those figures are so much worse for the average individual investor. A big reason for that is that many investors tend to trade emotionally and panic when the market drops also known as panic selling and then they try to time the market, or they jump in a stock as it’s going up for fear of missing out (FOMO investing) and it’s because of that, is why they usually end up getting much lower than average returns.

Also in a 2017 interview, the legend Warren Buffett went so far as to say that index funds make the best retirement sense “practically all the time”. Really, attempting to pick times to buy and sell stocks is a mistake for 99% of the population. Warren Buffett even went so far as to bet a collection of hedge fund managers $1,000,000 that they couldn’t beat the market over a ten-year period and outperform an index fund, and he won. A standard low cost Vanguard Index Fund beat some of the most highly paid (and expensive) fund managers.

Liquidity of Index Funds

Like we touched on earlier the liquidity of Index Funds is something you need to be aware of and it can actually be a double edged sword. Yes it may be slower to get money in and out of the fund when compared to the stock market. However if you are someone who tends to panic and watch prices constantly, this lower liquidity could actually help you not make big mistakes like selling if the price dips a bit. Furthermore there is a benefit here in that you can set up automatic transfers from your bank account directly into the Index Fund and you don’t need to worry about placing orders which you can’t do with an ETF on the stock market. This makes Index Funds a very hands free autopilot investing strategy which is great for the vast majority of investors when thinking about Index Funds vs ETFs vs Mutual Funds.

Exchange Traded Funds (ETFs)

Moving onto ETFs which are the newest form of these 3 investment funds, ETF stands for Exchange Traded Fund and this is exactly what it is. An ETF is a fund that, instead of buying into their fund through bank transfers, you can purchase portions of the fund directly on a stock exchange. If you want to know more about ETFs in particular check out my in-depth guide on getting started with ETFs.

ETFs can be both passively and actively managed but the vast majority of ETFs on the stock market are passive index tracking ETFs. Because of this a lot of time you’ll hear the terms ETFs and index funds used interchangeably but they’re not the same thing. If you wanted to invest in the S&P 500 you could either go with an S&P 500 Index fund like the Vanguard one that I mentioned earlier, or you can go with Vanguard’s ETF version of the same Index Fund.

A cool thing about ETFs is that they will usually have lower management fees than their corresponding Index Fund. In the US with the Vanguard S&P 500 Fund, the Index Fund version like I mentioned has a fee of 0.04% p.a but the ETF version has an even lower fee of 0.03% p.a.

The downside of ETFs is that they typically come with trading costs associated with the brokerage you pay to buy and sell stocks. However depending on which country you are in and which broker you are using this can be quite low or even nothing which would remove this downside. But, and this is something most other people have failed to mention when covering this topic, Index Funds also have costs associated with buying and selling and these can often be comparable to brokerage you are paying. It’s called the Buy / sell spread cost and is usually around 0.05%, so make sure you are aware of this when deciding what to use.

As I mentioned earlier ETFs trade just like stocks and so you can buy one share of an ETF at whatever price it’s trading at whether it’s a hundred dollars or whatever and you are now invested in that fund. So unlike Index Funds there is no minimum balance requirement with ETFs as long as you have enough money to purchase 1 share but if you don’t then you may be out of luck.

With an index fund you can buy fractional shares without much hassle. Some brokerages actually allow you to buy fractional shares of an ETF but others do not. So if you ever need to move your money to a different brokerage, how these fractional shares are treated can get really complicated so always check with your brokerage to see what they will allow and be aware that things can get a little complex if you ever need to move your money.

Which brings me to my next point on why ETFs are a bit more flexible than Index Funds. You can actually transfer your ETFs between different stock brokers if you want, without triggering a capital gains event. However with Index Funds you are stuck with your money in that account and the only way to move it would be by selling units which would trigger a possible capital gains event, which means you may need to pay tax at a non-ideal time.

Personally I purchase all of my investments through ETFs now. When I first started investing I actually started out with Vanguard Index Funds but these higher fees really start adding up over time and the spread between them in Australia is actually huge. The Vanguard Australia Shares Index Fund has management fees starting at 0.75% p.a, when the equivalent ETF on the ASX VAS only has a fee of 0.10% p.a, 7 times lower! Also, and I’m not sure if this has changed now but when I wanted to withdraw my funds from the Vanguard Index Fund, the only option was to fill out a paper form and mail it to their office, which then took about 2 weeks to finally get my money.

Ultimately the best one for you is going to depend on what you’re actually trying to achieve. If you’re someone who tends to panic sell and you don’t really need access to money quickly than using an Index Fund instead of an ETF might be better, even if the fees are slightly higher. However if you want a small chance of beating the overall market with a guaranteed chance of paying higher fees then you might want to look at actively managed Mutual Funds when thinking about Index Funds vs ETFs vs Mutual Funds.

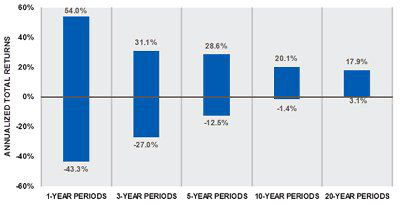

But in saying that there have been dozens if not hundreds of studies that have been done on this that proved that time in the market beats timing the market in the majority of situations and a study done by Charles Schwab in 2012 found that between 1926 and 2011, a 20 year holding period across broad market ETFs NEVER produced a negative return.

No one can predict what the market is going to be doing in the short term so why even try instead I just invest whenever I have the money with the expectation of holding it one to two decades and I will come out ahead now in terms of actually doing this it is really just as simple as going to opening a stock market brokerage or index fund account and keep buying the same investments over and over and over again and expect to grow your wealth at the same rate as the entire stock market. And that’s pretty much it that’s all you have to do it’s really easy it’s really basic it’s really simple and that strategy will be perfect for 99% of individual investors out there for a very low cost I mean it’s really just there’s nothing not to like about this.

So with that said you guys thank you so much for reading I hope you find this overview of Index Funds vs ETFs vs Mutual Funds useful. Let me know in the comments if you have any questions or if there’s a topic you would like me to cover next.